Behavioral Side of Total Supply and Price per Token

This article explains the behavioural side of total token supply and price per token: how different supply choices affect price perception, why ultra-low prices below $0.01 often underperform, and how emissions and allocations can either support or destroy your token’s long-term performance.

This article is the second part of series to learn more about Tokenomics from author & contributor: Max K - CEO Coinstruct.tech. Read the first part here: Supply-Side Tokenomics: Supply, Distribution, Optimization for Price Performance & Cost-Efficiency

TL;DR — Behavioral Side of Total Supply and Price per Token

The absolute number of tokens in your total supply (10M vs 1B vs 100B) matters far less than most founders think. What really drives long-term performance is how total supply translates into price per token at a given market cap, how retail investors perceive different price buckets, and how emissions and allocations interact with that behaviour. Tokens priced below $0.01 tend to underperform and be more volatile, extreme low prices with many zeros confuse users, and poorly designed emissions often create “built-in” dump conditions. This article explains how to choose total supply, price ranges and emission curves that work with human psychology instead of against it.

Defining Total Token Supply and Its Impact on Price

Once you've opted for a capped maximum supply, the next step - is to define the exact number of tokens. 10M, 100M or even 100B tokens as your total supply?

The answer, which may not align with expectations, is that the choice holds relatively little significance—aside from leveraging psychological biases, the selected number is essentially random.

There exists no specific reasons dictating why Bitcoin had to be designated with a 21 million maximum supply. It could have just as viably been 2.1 million, 210 million, or any other figure. However, Satoshi Nacomoto is known to be targeting future Bitcion price to be the similar value to many popular fiat currencies, so it would be more comfortable to execute transactions. The primary impact of the maximum supply is actually observed in its influence on the price per token within a given market capitalization (MC).

Take a moment to subscribe to our weekly web3 digest. We curate a special web3 digest packed with useful tools, market insights, and exclusive opportunities tailored for founders and investors.

Defining Token Price per Unit and Investor Perception

The price per token is another psychological issue that slightly affects the perception of many retail investors and sometimes even influences the price performance.

Some interesting insights can be driven from TradFi. The price per share, akin to the price per token, holds no intrinsic value and provides little insight to a rational investor regarding the company's relative worth, recent performance, or anticipated future performance. Still, there is a tendency for stocks to experience significant growth subsequent to stock splits. Stock splits result in a reduction in the price per share alongside an increase in the number of shares, while maintaining the market capitalization and dilution at constant levels. For instance, in a 1:10 split, if an investor owns 1 share priced at $100/share before the split, they would own 10 shares priced at $10/share afterward, yet the $100 investment still represents the same proportion of ownership in the company in both scenarios. This phenomenon of outperformance post-splits may be attributed to investors' irrational preference for lower-priced shares.

The same approach seems to be taking place with tokens. Although these perception biases typically imply that a lower token price is more favorable, it stands to reason that there is likely a limit to this advantage.

For instance, if consumers attach greater significance to the leftmost digit, there is probably a substantial psychological gap between a token priced at $0.01 and one at $1.00, compared to the difference between $0.000001 and $0.0001, despite both representing a 100x increase. When individuals find themselves needing to pause and carefully count leading zeros, it suggests that the price may have surpassed the optimal point to benefit from any bias towards lower prices.

At Coinstruct, after analyzing top 1000 projects by Market Cap, we found out that the findings roughly seem to reject the “lower price is better” hypothesis. The $<0.01 price per token range had statistically significantly worse returns than the ≥$10 - <$100 price range.

Tokens priced below $0.01 exhibit a statistically significant higher volatility in relative monthly returns compared to tokens priced between $1.00 to less than $10.00, tokens priced above $100.00, and tokens priced between $10.00 to less than $100.00. This indicates a consistently wider range of performance relative to the market across different price buckets.

For builders, this suggests the importance of avoiding selecting a maximum supply that would result in an expected token price below $0.01. Below this threshold, the data indicates that tokens tend to underperform significantly and may experience heightened volatility. This phenomenon could be attributed to psychological perceptions of tokens priced below 1 cent as high-risk, or perhaps due to the presence of a large number of low-quality coins attempting to leverage a low token price as a marketing gimmick.

💡 Before you decide whether your token should trade at $0.1, $1 or $10 at listing, model what this means for FDV, initial market cap and investor allocations.

We built a Tokenomics Calculator PRO that lets you play with total supply, listing price and unlocks to see how different choices change your numbers.

Optimizing Token Emissions and Vesting for Sustainable Price

What should developers consider when determining their emission curve?

The data indicates that optimizing emissions doesn't solely revolve around minimizing inflation at any expense, as often presumed by many builders. Instead, it's about striking a delicate equilibrium between supply and demand, establishing and sustaining the right incentives, defining valuable user actions, ensuring a well-distributed holder base, and fostering protocol stability—all contingent on the unique requirements of your project. There isn't a universal "optimal emissions curve," but rather a set of best practices and improvements over linear time-based models that warrant consideration.

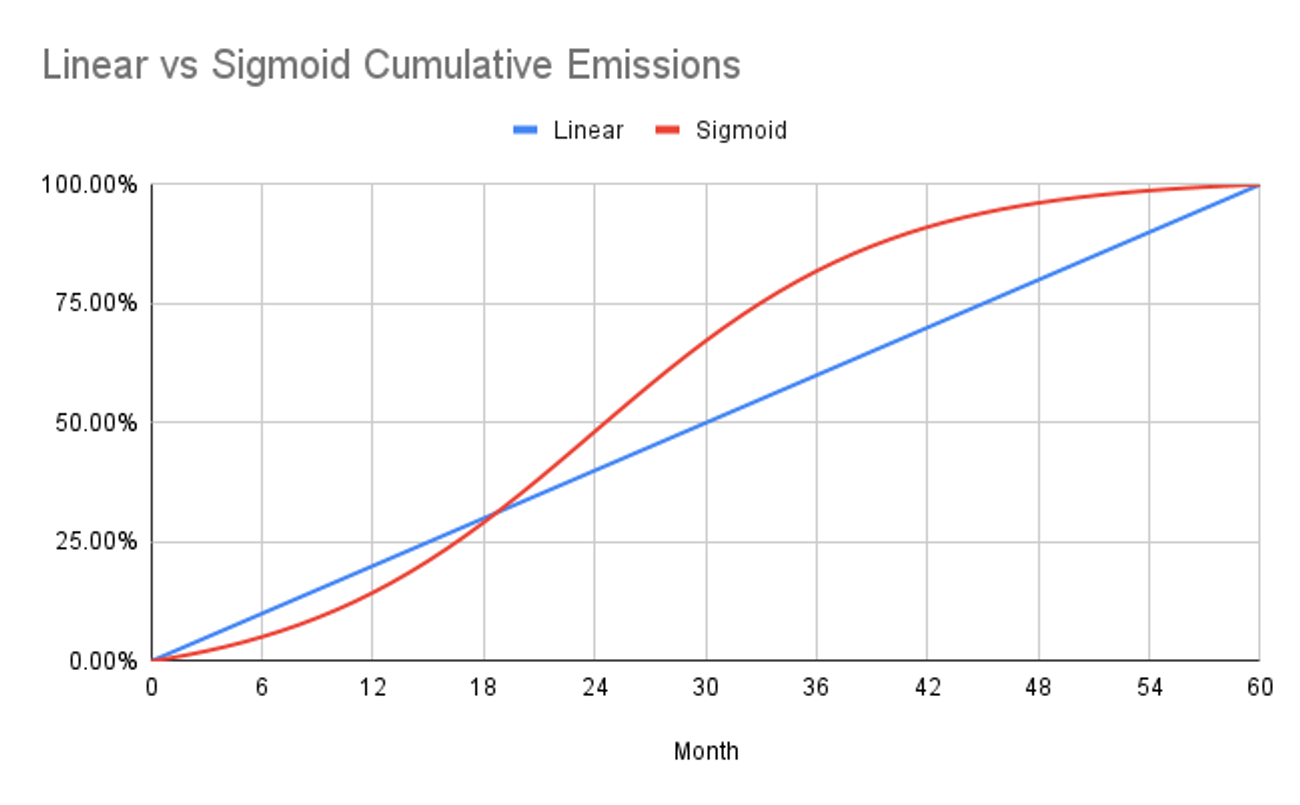

Usually vesting in crypto is time-based, which means that tokens are distributed after a set time period passes. However, vesting can also be done according to the project's progress, such as milestone vesting. In particular, utilizing "S"-shaped curves, such as the sigmoid curve depicted in the image below, may offer advantages over linear schedules.

As you can notice, the rates of inflation, or dilution, tend to be highest during the initial launch of a token due to the fact that the existing supply is at its lowest-ever levels. This holds true for most projects, even those employing linear emissions schedules. As a result, many projects experience their peak inflation rates at the start, setting the stage for optimal conditions for a price decline. This phenomenon can lead to the perception of the project as a pump-and-dump scheme. That’s why it is important to consider other supply curves rather than linear.

A finely tuned sigmoid curve diminishes inflation during periods when the project is particularly vulnerable to pump-and-dump schemes, effectively smoothing the inflation rate more evenly across the entire schedule. However, it's important to note that a curve cannot emit fewer tokens than an equivalently long linear curve without eventually emitting more tokens than the linear curve at some point.

This phenomenon is evident in the curve depicted above, where the month-to-month token emissions of the sigmoid curve surpass those of the linear curve from approximately Year 1 to Year 3 within the 5-year emissions schedule. Yet, this deviation from linearity may be deemed an acceptable trade-off for achieving lower inflation rates during the project's initial launch phase, and it might even represent an inherent strength of sigmoid curve emissions.

It is also worth looking at some profound vesting dynamics like AVV (Adoption Adjusted Vesting) proposed by Achim Struve. The main idea of this approach is to get rid of traditional time-based vesting schedules where the majority of the supply gets emitted into the ecosystem at the early building phase of the product suite. In other words a lot of supply hits low market demand.

AVV utilizes a flexible and smooth approach with algorithmic token vesting according to certain KPIs. AVV is determined by controllers that increase the emissions in lower adoption and decrease them in higher adoption phases. In this case vesting tokens could be issued into the ecosystem depending on TVL, user acquisition / token holder count, revenue thresholds, locking allocations, or the token price itself. Looking at the example of TVL the token vesting rate could be increased in phases of low protocol TVL to have more tokens to incentivise deposits through higher rewards.

Token Allocations Between Team, Investors, Treasury and Community

When launching a token, deciding on the recipients and distribution methods are among the pivotal tokenomics design choices. These crucial decisions hold significant sway over how your token is perceived and performs, serving as key indicators of whether the team and initial supporters have aligned incentives.

For a data-driven approach to allocation, we should look at what is typical for projects and generally best practice.

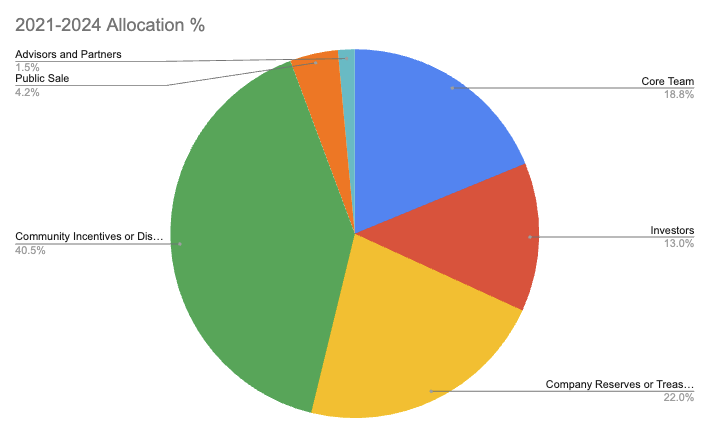

- For the Core Team, approximately 18.8% of tokens are set aside, encompassing allocations for founders, employees, and other contributors.

- The investor allocation stands at about 13%, though this average incorporates projects without investor presence, thereby reducing the overall category allocation. However, when exclusively considering projects with investor involvement, the token allocation percentage rises to 17%.

- Reserved for future product development and operational expenses, Company Reserves or Treasury funds hold approximately 22% of the token allocation.

- Community Incentives or Distributions hold the largest allocation at 40.5%. This elevated allocation is logical as it aids in achieving adequate decentralization and widespread network ownership. Additionally, it serves as the primary method to incentivize product usage and early engagement.

- A fraction of tokens, namely 4.2%, is designated for Public Sales, including public exchange listings and token sales. This figure has decreased from 55% in 2017, likely due to regulatory constraints, leading to a corresponding uptick in allocations to investors and community incentives.

- Lastly, partners and advisors typically receive an allocation of 1.5% of tokens.

With that being said, no “one-size-fits-all” token allocation exists for all crypto projects. Every project should tailor their token allocation plan to match its unique internal economic system.

Behavioral Side of Total Supply & Price - FAQ

What is “total token supply” and why does it matter?

Total token supply is the maximum number of tokens that can ever exist for your project. On its own, the absolute number (10M vs 1B vs 100B) does not change the fundamental value of the network. However, it directly affects the price per token at a given market cap and how investors perceive that price, which can drive very different behaviours in the market.

Does a higher total supply make my token “cheaper” and more attractive?

Not really. A higher total supply simply spreads the same market cap over more units, lowering the price per token. Retail investors often like “cheap-looking” tokens, but our data shows that extremely low prices (especially below $0.01) are correlated with worse returns and higher volatility. Many low-quality projects use huge supplies and tiny prices as a marketing gimmick.

Is it a good idea to launch with a token price like $0.000001?

In most cases, no. Prices with many leading zeros are harder for users to reason about, create unrealistic “I’ll be rich if it ever goes to $1” expectations and tend to behave more like lottery tickets than serious assets. The psychological gap between $0.01 and $1.00 is much more meaningful than between $0.000001 and $0.0001, even though both represent a 100x move.

What is a healthy price range for my token at launch?

There is no perfect magic number, but you should avoid designing total supply in a way that pushes the expected price per token below $0.01. Aim for a range where the price looks intuitive and comparable to other quality assets in your vertical, while keeping FDV realistic and aligned with fundamentals. Price should help investors anchor expectations, not be a pure marketing trick.

How do total supply and emissions interact with investor behaviour over time?

Total supply and the initial price set the psychological frame for your token. Emissions and vesting schedules then determine how quickly new supply hits the market relative to real demand. If a large part of your supply unlocks into a weak market, or if early insiders receive a lot of tokens when retail liquidity is thin, this creates constant sell pressure and reinforces “dump” behaviour. Well-designed emissions smooth out inflation and align unlocks with real adoption.

Coinstruct is an official tokenomics partner of InnMind. It has developed 25+ tokenomics including such projects as Nomis Protocol (LayerZero, zkSync, Galaxe partner), Otcmarsbase.io (+$450M in Published Deals), AANN.ai (+$1M raised), Dexodus.xyz, it's consulted projects such as InnMind.com ($60M raised by Startups), Claimr, CryptoDo, Pictographs (Linea partner), Qoomon Quests (team from Goldman Sachs and Tencent) and 20+ more across various blockchain ecosystems. Coinstruct team know how to approach tokenomics challenges with all the supply & demand factors.

Coinstruct is a specialized agency for full-cycle Web3 tokenomics development where we have a team of diverse specialists from mathematicians, product managers to degens from leading DAOs working together to create advanced token models, reward systems, economy audits and scoring. Our focus is to create Web3-native sustainable economic solutions to help projects achieve desired goals through tokens: from efficient fundraising to increasing user base, retention and loyalty.

Don't forget to join our new Telegram channel when we share tokenomics insights and experience.

Read also:

Nelli Orlova

Nelli Orlova Alex Onishenko

Alex Onishenko