How Not to Bank: Lessons for Web3 Startups from Silvergate Shutdown and SVB Bank Run

Banking.

This is one thing that crypto wanted to change right from the start.

I mean think about the buzzwords + phrases:

“Bank the unbanked”

“Decentralized banking”

“Banking for the new digital economy”

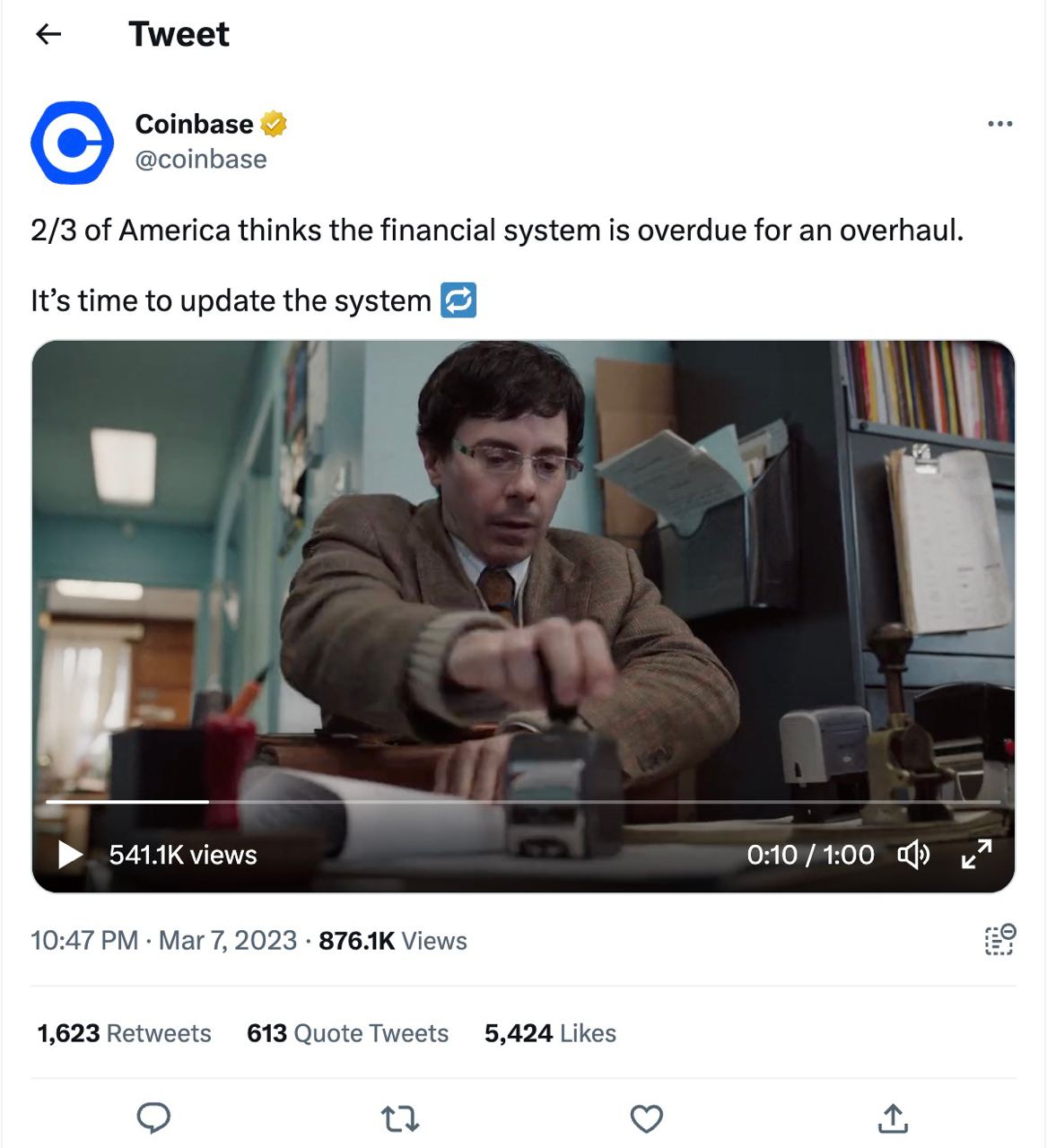

Coinbase, the shining regulated multi-billion light of the crypto industry (btw: we have an early Coinbase pitch deck from the seed funding round here) literally released a video last week decrying the traditional financial system.

I'd give them:

- 10/10 for the script

- 10/10 for the acting + narration

- But most of all 0/10 for the timing.

I mean THIS ☝️ couldn’t have been timed any worse than it did.

- 🗓️ March 8: Coinbase drops the video

- 🗓️ March 9: Crypto bank Silvergate Bank shuts down

- 🗓️ March 10: Startup bank Silicon Valley Bank shuts down

- 🗓️ March 11: Coinbase and Circle’s stablecoin USDC depegs to 0.9 per $1

Alexa, play “What Goes Around... Comes Around” by Justin Timberlake

The problem at the centre of all this is → Banking.

Anyone surprised? 😳

Not crypto banking or decentralized banking or even centralized banking.

It’s this kind of banking. The risky kind. 🥵

It’s the same kinda banking that was at the center of:

- FTX

- Terra

- Celsius

- Every nightmare for the past year

Okay, I got a little carried away there lol.

It’s risky banking.

Okay, let’s be real for a minute. Banking is all about one thing – taking money from one party and giving it to the other party.

🫴 Taking money from one party = Lenders (people who don’t need it now)

🫳 Giving money to the other party = Borrowers (people who need it now)

Alright, this is an oversimplification. But you geddit right?

And herein lies the problem for – both Silvergate and SVB – and how they fell into the same trap.

The trap of risky banking. It’s not just a risk of whom they gave the money to, but the risk of when they gave the money.

- → Silvergate – was the banking partner of major crypto exchanges.

- → SVB – was the banking partner of major technology startups.

And who was on the other end of these banks?

Simple 💡

Anyone who loved risk.

But different degrees of risk.

Hey! My kinda risk is saying F it and hitting the “I’m feeling lucky” button on Google searches. That’s a big risk for me. But to people who jump outta airplanes for “the thrill,” it seems whatevs.

For Silvergate:

The ones on the other side were – retail and institutional investors – apeing into crypto via exchanges and decentralized finance protocols.

For SVB:

The ones on the other side were – venture capitalists – funding every small and large technology startup in Silicon Valley and across the world through accelerators and regional funds.

Q. What was the goal of these investors?

A. Massive returns.

👉 Investors wanted to make bank apeing into crypto.

👉 VCs wanted to make bank investing in startups.

And this euphoria started in 2020 – when Covid-19 started.

At the time, the governments went, ‘Alright. Start the printers, let's shock the economy into working again.’

And then they began to pump money into the market.

→ 🚀 When everything was going up, getting these returns was hella easy

→ 💩 Other investments (like treasury bills and bonds) were not yielding squat

The economic term for this is – low-interest rates.

The euphoria ended when governments went, ‘Alright. Stop the printers, let's start the burners.’

And then they began to pull back all the money they pumped into the market.

That’s right. Unlike a game of Uno at my house, the world economy has “backsies” 😭

The economic term for this is – raising interest rates.

When rates go up – everyone wants to lock their money in a bank account or a government bond.

And relatively, no one wants to invest in something as risky as a healthtech company using ChatGPT to do cardiac surgery (idk if such a thing exists, but if it does a VC will find it and invest in it) or doggy coins. You know the eternal VC dilemma. 🤷♀️

That’s what happened about ~6 months ago.

For crypto, the telltale sign was the collapse of FTX.

But for tech, the signs were less one major company failing and more a buncha scattered companies laying off thousands.

🗓️ 2022 → 160k employees were laid off

🗓️ 2023 (so far) → 128k employees were laid off

And that’s when VCs (and everyone else who funded these companies) realized – maybe it’s not the best time to invest in thousands of high-risk technology startups that burn money for years only for a handful to make it out alive. Just maybe 🤣

This started happening a few months ago

And it all came to a head last week.

- Silvergate shutdown because customers of crypto exchanges were pulling their money faster than I pull out…of the McDonald’s drive-thru when I see an extra chicken nugget in my meal

- SVB is seeking regulatory help because VCs are not funding startups making the [borrowed] cash rich, and hence they gotta withdraw money to keep doing da business

Silvergate and SVB didn’t have anything directly to do with each other (well maybe it did, you never know lol).

But their downfall is similar. Very similar.

Both lent money to people who took big risks which paid off when money was cheap but didn’t when money suddenly wasn’t so cheap.

So, what’s the lesson for web3 companies in this space?

Eh for starters, don’t name your company something cringe like – Silicon Valley Bank or Silvergate Bank.

Keep it on the DL, something like “Money? Never heard of him Bank” or “Empty Pocket Capital.”

But the larger picture is – taking risks with borrowed money is not a good idea. And relying on borrowed money (even if it’s investments) is not a good idea too.

Instead, build products that can thriftily scale or can generate cash on its own.

And when you’re taking custody, custody [a good chunk of] it with yourselves.

You never know – your bank or your investor – might be more broke than you are.

🙃

PS: Tweet this post if you like it and wanna share your ❤️!

Web3 founders also love:

Nelli Orlova

Nelli Orlova

InnMind

InnMind Val Baev

Val Baev